Payday Super Australia 2026: The Complete Employer Guide to Qualifying Earnings, SGC, STP and Staying Fine-Free

From 1 July 2026, Australian employers move into a new super compliance reality. Quarterly super timing is no longer the practical benchmark. Under Payday Super, employers must pay super guarantee at the same time as salary and wages and ensure the contribution is received by the employee's super fund within 7 business days, unless an extended timeframe applies. This is one of the biggest payroll and compliance shifts Australian businesses have faced in years, and it affects cash flow, payroll governance, reporting discipline, employee data quality, and risk exposure at the same time.

For many employers, the change will sound simple at first. Pay super on payday. In practice, it is much larger than that. The reform changes how super is calculated, what earnings base is used, what must be reported through STP, how missed or late payments are assessed, and how quickly payroll teams must resolve errors before they become chargeable events. It also removes old habits that many businesses relied on, including long quarterly timing buffers and legacy workflows tied to the Small Business Superannuation Clearing House.

This article gives you the full business level explanation. It covers how Payday Super works, what qualifying earnings mean, how the new super guarantee charge operates, what the ATO uses to calculate whether you paid enough and on time, how SuperStream is changing, where many employers are likely to fail, and how a proactive system like BizbellDesk.com can help businesses stay alert and avoid penalties before they happen.

In This Guide

- What Payday Super actually means

- Why this change is bigger than many employers think

- Qualifying earnings explained in simple language

- How the ATO uses STP and super fund data

- The new super guarantee charge and penalty risk

- SuperStream upgrades and payment workflow changes

- What employers should do before 1 July 2026

- How BizbellDesk helps companies stay compliant

- Frequently asked questions

What Payday Super actually means

Payday Super changes two things that matter immediately. First, the timing of payment. Second, the earnings base used to calculate the minimum super guarantee amount.

Under the new rules, the employer must make the super contribution for eligible employees on payday, at the same time as paying salary and wages. That contribution must be received by the fund within 7 business days, unless a longer period applies in limited cases such as some new employee scenarios. It is no longer enough to think in quarters and assume a later sweep will fix the issue.

The second shift is the move to qualifying earnings, often shortened to QE. From 1 July 2026, employers use QE as the base to calculate both the super guarantee amount and the new SGC logic. That means the operational payroll layer and the compliance layer become much more tightly linked.

Why this change is bigger than many employers think

Many businesses still treat super as a periodic finance task rather than a real time compliance system. That approach becomes dangerous under Payday Super. The old quarterly window gave employers more room to fix mistakes. The new model is tighter. Super now sits much closer to your actual payroll engine, employee records, clearing workflow, and payment rails.

That means five business functions suddenly matter more:

- Payroll timing, because STP reporting is due on or before the day you pay employees.

- Employee master data quality, because invalid fund details, name mismatches, or account errors can delay contributions.

- Cash flow planning, because super leaves the business more frequently.

- Error handling speed, because rejected or incomplete contributions must be corrected quickly.

- Governance visibility, because management needs to know which employees, pay cycles, and liabilities are exposed.

In short, Payday Super is not only a payroll rule. It is an operating discipline. Employers that treat it as an admin change will struggle. Employers that treat it as a workflow, data, and compliance system will cope much better.

Qualifying earnings explained in simple language

One of the most important terms in the new model is qualifying earnings. QE is the payment base used from 1 July 2026 to calculate the super guarantee amount.

In practical terms, QE includes key earnings categories such as ordinary time earnings, all commissions, some salary sacrifice amounts that would have counted if paid directly, and payments to some workers who fall within the expanded employee definition for super purposes, including some contractors paid mainly for their labour.

This matters because many employers are used to thinking in older payroll categories only. With Payday Super, your payroll coding, pay items, and reporting setup need to reflect the correct treatment of QE. If those settings are wrong, your reporting may be wrong. If reporting is wrong, your apparent super obligation may be wrong. If your obligation is wrong, the business can face follow up action, corrections, or assessment problems.

It also matters because not every payment category behaves the same way. Some items can still sit outside QE even where a separate industrial instrument requires super to be paid on them. That means businesses cannot rely on guesswork. Their payroll mapping has to be deliberate.

Examples that help employers think correctly

If an employee is paid ordinary hours, that will generally sit inside QE. If an employee receives commissions, those commissions are included. If a contractor is mainly paid for labour and falls within the super definition, that payment may also matter. On the other hand, some categories that are treated differently under industrial obligations do not automatically become QE just because super may still be payable for a separate reason.

The key lesson is operational. Payroll teams need correct classification before the day of payment, not after. Waiting until reconciliation stage is too late in a 7 business day environment.

How the ATO uses STP and super fund data

The ATO has explained that it uses two main data streams to work out what you owe and whether you paid it on time: Single Touch Payroll data and super fund data.

Your STP report is due on or before the day you pay employees. From 1 July 2026, employers must report year to date qualifying earnings amounts for each relevant employee. The ATO then uses that year to date amount to determine the QE amount for a specific payday by subtracting the previous period's YTD QE from the current period's YTD QE.

That means the ATO does not need you to report each payday amount as a separate standalone field in a simple one line way. It can derive the current payday QE from the difference between one YTD figure and the next. Once the QE amount for that payday is determined, the expected individual super amount can be calculated by applying the applicable SG rate. For the 2026 to 2027 year, that rate is 12%.

Then the second data stream comes in. When you pay the super, the fund reports payment information, including when it was received. This is what helps determine whether you met the minimum SG for the employee and whether you did so on time.

Why inconsistent data becomes a serious business risk

The ATO has also flagged cases where the data it holds may not align with employer records. This can happen if contributions are paid without all required SuperStream information, if the ABN used in contribution messaging does not line up correctly with the STP reporting ABN, if employee matching fails, or if reporting is late, incomplete, or inaccurate.

This is where many businesses will get caught. Not because they intended to underpay super, but because their data chain was weak. A payroll team might think the money was sent. The fund may have received something incomplete. The data may not match. The allocation may fail. The employer then assumes the job is done, while the compliance clock continues to run.

That is why record quality and exception management matter just as much as paying the amount itself.

| Compliance Element | What the ATO uses | Risk if weak |

|---|---|---|

| Payday and earnings reporting | STP YTD QE and super liability data | Wrong expected SG amount, mismatch, follow up |

| Contribution receipt timing | Super fund reported receipt date | Late contribution exposure |

| Employee identity and fund data | SuperStream and fund validation details | Rejected or unallocated payments |

| ABN consistency | STP and contribution message alignment | Matching problems and compliance uncertainty |

The new super guarantee charge and penalty risk

Under the Payday Super model, the super guarantee charge becomes more structured, more data driven, and more serious from a risk management perspective. The ATO has outlined that the new SGC is assessed by it, rather than being handled in the same way many employers are used to under the older system.

For each QE day, which is effectively payday, the charge can include four components:

- the total of individual final SG shortfalls

- the sum of notional earnings

- any administrative uplift amount

- any choice loading, where relevant

This matters because the cost of missing super is no longer only about the unpaid amount. The liability can grow through additional layers.

How shortfalls arise

For each employee on a QE day, there is an individual SG amount. That is the minimum super that should be paid. If enough contribution reaches the fund on time, the base shortfall can be zero. If it does not, the base shortfall exists. If a late contribution is made before the ATO assessment, that late contribution can reduce the final shortfall, but the issue is still not the same as having paid on time.

Notional earnings increase the pain

Notional earnings are calculated using the general interest charge rate and compound daily. That means delay costs money, and delay compounds. This is why businesses should stop thinking that a short miss can always be cleaned up cheaply later. Under the new logic, time matters far more.

Administrative uplift and choice loading

The ATO has also explained an administrative uplift concept and a possible choice loading where the choice of fund rules have not been followed. That means super compliance is not only about sending money. It is also about following the process correctly.

Late payment penalties can still escalate

If an SGC assessment is issued and remains unpaid after the required period, a late payment penalty can apply. The penalty is generally 25% of the outstanding SGC amount and can rise to 50% if there has been prior liability within the previous 24 months. The ATO states that this late payment penalty cannot be remitted.

SuperStream upgrades and what they mean for payroll teams

SuperStream is also changing from 1 July 2026, and these changes matter because they support the new deadline model. The ATO has explained that upgraded messaging and workflow changes are intended to reduce rejected contributions, improve error messaging, enable faster payments, and give earlier notice about important fund detail changes.

Three practical upgrades matter most for employers.

1. Better validation before the payment goes wrong

A new member verification request capability is designed to help verify whether employee super fund details are valid and whether the fund can accept the contribution. This gives businesses a chance to catch problems earlier, especially where employee details have changed or a previous contribution has been rejected.

2. Better error messaging

Historically, payroll and finance teams often receive vague warnings that are easy to ignore. Under the upgraded environment, clearer and faster error messaging should improve the ability to fix problems quickly. That is critical in a 7 business day environment.

3. Faster payment rails

The New Payments Platform can help contributions reach super funds faster, potentially even on the same day in some cases, depending on the provider path. This does not mean every payment route is instant, but it means employers must understand their actual provider timing rather than guessing.

If your payroll provider, clearing house, or payment process takes extra time, that internal lag is now your business problem. A contribution that leaves your bank account too late can still be late if it reaches the fund after the deadline.

What employers should do before 1 July 2026

The smartest employers are not waiting until July. They are preparing now. Based on the ATO's checklist logic and the practical risk points above, here is the business version of the readiness plan.

1. Review payroll governance now

Check every part of the payroll to super chain. Who approves payroll. When STP is lodged. When super files are created. Which provider transmits them. How exceptions are handled. Who confirms the fund received the contribution. If there is no clear answer for each step, you have a governance gap.

2. Audit employee and fund data

Bad data will become expensive. Review member numbers, USIs, employee names, fund details, default fund details, and any known rejection patterns. Fix them now.

3. Review cash flow rhythm

Quarterly thinking must shift to payday thinking. This affects cash buffers, settlement timing, and payroll funding discipline. Employers need to forecast the impact of more frequent super outflows.

4. Confirm software readiness

Your digital service provider should confirm when its system will support QE reporting, new error flows, and any SuperStream updates needed. Ask direct questions. Do not assume the system will simply be ready.

5. Understand the SBSCH transition

The SBSCH is no longer a long term answer. New users were cut off earlier, existing access ends by 30 June 2026, and from 1 July 2026 it is no longer available. Businesses still relying on it need to move.

6. Build a fast correction process

Errors will still happen. The difference between a fine and a fix may come down to whether your business can detect and resolve the issue quickly. Create a same day or next day exception workflow.

7. Watch labour only contractor exposure

Some businesses assume contractors sit outside super by default. That assumption is unsafe. Where workers are paid mainly for their labour, super rules may still apply. Review those engagements carefully.

How BizbellDesk.com turns Payday Super into a visible compliance system

This is where software and business model design matter. The biggest Payday Super risk for employers is not just the law itself. It is the gap between legal duty and day to day visibility. Many business owners do not miss obligations because they do not care. They miss them because the process is scattered across payroll, spreadsheets, emails, fund portals, and late human follow up.

BizbellDesk.com has built a solution model for companies that need a clear operating view instead of fragmented reminders. The goal is simple: keep employers awake, give them a live liability picture, and stop missed super from turning into avoidable fines.

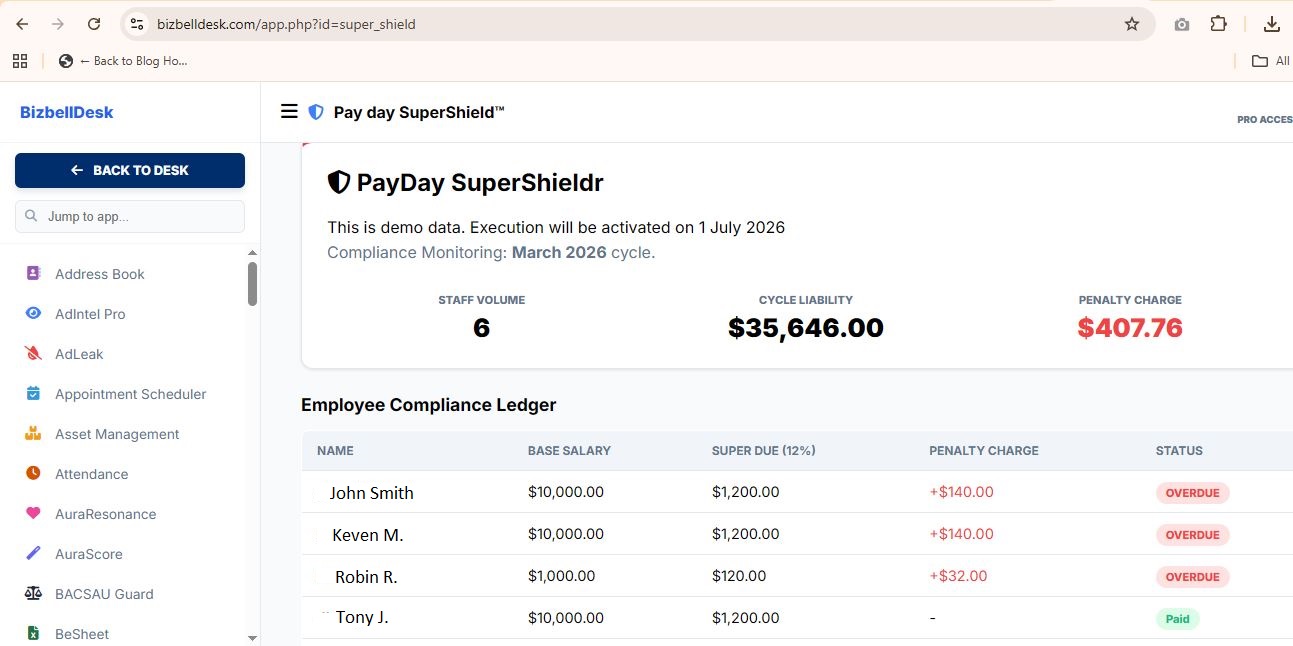

As shown in the dashboard concept above, BizbellDesk's PayDay SuperShield model focuses on operational clarity. Instead of burying risk inside payroll exports, it surfaces key decision points at a glance:

- Staff volume, so the employer immediately knows the compliance footprint for the cycle.

- Cycle liability, so the super amount in play is visible before it becomes a due date issue.

- Penalty charge exposure, so management sees the cost of delay in commercial terms.

- Employee compliance ledger, so each worker can be tracked as paid, overdue, or at risk.

That business model matters because Payday Super is no longer only a finance back office task. It is an executive risk item. Directors, business owners, payroll leads, finance teams, and operations managers all need the same source of truth. A dashboard that shows only totals is not enough. A spreadsheet that updates once a week is not enough. What businesses need is a cycle by cycle compliance cockpit.

BizbellDesk's approach is powerful for three reasons.

First, it converts legal language into visible business signals

Most employers do not think in terms such as individual final SG shortfall or notional earnings. They think in questions like: who is overdue, how much is exposed, what is the penalty risk, and what must be fixed today. Good compliance software translates law into action. That is exactly where a product like PayDay SuperShield becomes useful.

Second, it supports operational discipline

When every payday is a compliance event, businesses need repeatable cycles. A system that shows which contributions are due, which were sent, which remain unconfirmed, and which employees are exposed can reduce reliance on memory and manual chasing.

Third, it helps directors and owners make earlier decisions

If an owner sees a rising cycle liability, overdue statuses, and growing penalty exposure before an assessment is triggered, they can act sooner. This is the difference between compliance management and damage control.

For Australian companies with multiple staff, mixed pay cycles, labour hire patterns, or thin admin capacity, this kind of model is likely to become far more valuable after 1 July 2026.

Why authority articles on Payday Super must go beyond the law summary

Many pages online will repeat the headline facts. Payday Super starts 1 July 2026. Super must be paid on payday. QE replaces the older base. STP will include QE. That is useful, but it is not enough for business decision makers.

A real authority resource must explain what happens inside the business. It must show where employers fail, where data breaks, where software matters, where cash flow tightens, where contractor assumptions become dangerous, and where management visibility can stop fines before they happen. That is why a serious employer guide should combine official compliance points with practical operating advice.

This is also why BizbellDesk fits naturally into the conversation. It is not presented as a legal authority. The ATO remains the official authority. But BizbellDesk is positioned as the practical operating layer that helps businesses manage their internal workflow so they can meet that official standard.

What business owners should remember most

If you remember only five things from this guide, make them these:

- From 1 July 2026, super moves much closer to each payday.

- Contributions must be received by the fund within 7 business days, unless a longer period applies.

- Qualifying earnings now matter because they drive the SG base and related compliance logic.

- The ATO uses STP and fund data together, so reporting quality and payment quality both matter.

- Businesses that do not build visibility will be more exposed to shortfalls, charges, and penalties.

Frequently Asked Questions

When does Payday Super start?

Payday Super starts from 1 July 2026 for relevant super guarantee payments. Employers need to be ready before then because payroll, fund data, reporting, and payment workflows all need to line up from day one.

Do I still have 28 days after quarter end?

For periods covered by Payday Super, the focus changes to each payday. The key rule is that the super contribution must be received by the fund within 7 business days of payday, unless a longer period applies.

What is QE in simple terms?

QE means qualifying earnings. It is the earnings base used from 1 July 2026 to calculate minimum SG and related SGC obligations. It includes important payment categories such as ordinary time earnings and commissions, plus some other amounts specified in the new framework.

What if my contribution is sent but rejected?

If the contribution is not correctly received and able to be allocated by the fund in time, the business can still face late payment exposure. That is why employee data quality and fast correction workflows matter so much.

What happens to the SBSCH?

It is no longer a long term option. Existing users only have access until 30 June 2026, and from 1 July 2026 it is no longer available. Businesses still relying on it should transition now.

How can BizbellDesk help?

BizbellDesk can help by turning Payday Super into a visible compliance dashboard. Instead of waiting for a missed payment to become a penalty event, employers can monitor staff volume, cycle liability, overdue records, and estimated penalty exposure in one place.

Final verdict

Payday Super is one of the most important payroll compliance changes Australian employers have faced in recent years. It tightens timing, strengthens data dependency, increases the importance of accurate STP reporting, and raises the commercial cost of delay. Businesses that still treat super as an afterthought are likely to feel the pressure. Businesses that build strong workflow, clean data, faster correction processes, and real visibility will be far better positioned.

The law sets the standard. Your internal system determines whether you meet it consistently.

If your company wants a practical way to stay alert, surface risk early, and avoid slipping into avoidable fines, review how BizbellDesk.com is building compliance focused models such as PayDay SuperShield. In a Payday Super world, calm visibility is no longer a luxury. It is a business control.

Build your Payday Super compliance layer before July 2026

Explore BizbellDesk and see how a live liability dashboard, employee compliance ledger, and penalty visibility model can help your business avoid missed super and reduce compliance stress.